Managing taxes can be complex for small business owners and professionals. To simplify taxation, the government introduced the presumptive taxation scheme under Sections 44AD and 44ADA of the Income Tax Act.

Understanding presumptive taxation scheme 44AD 44ADA helps you reduce compliance burden, save time, and file taxes easily.

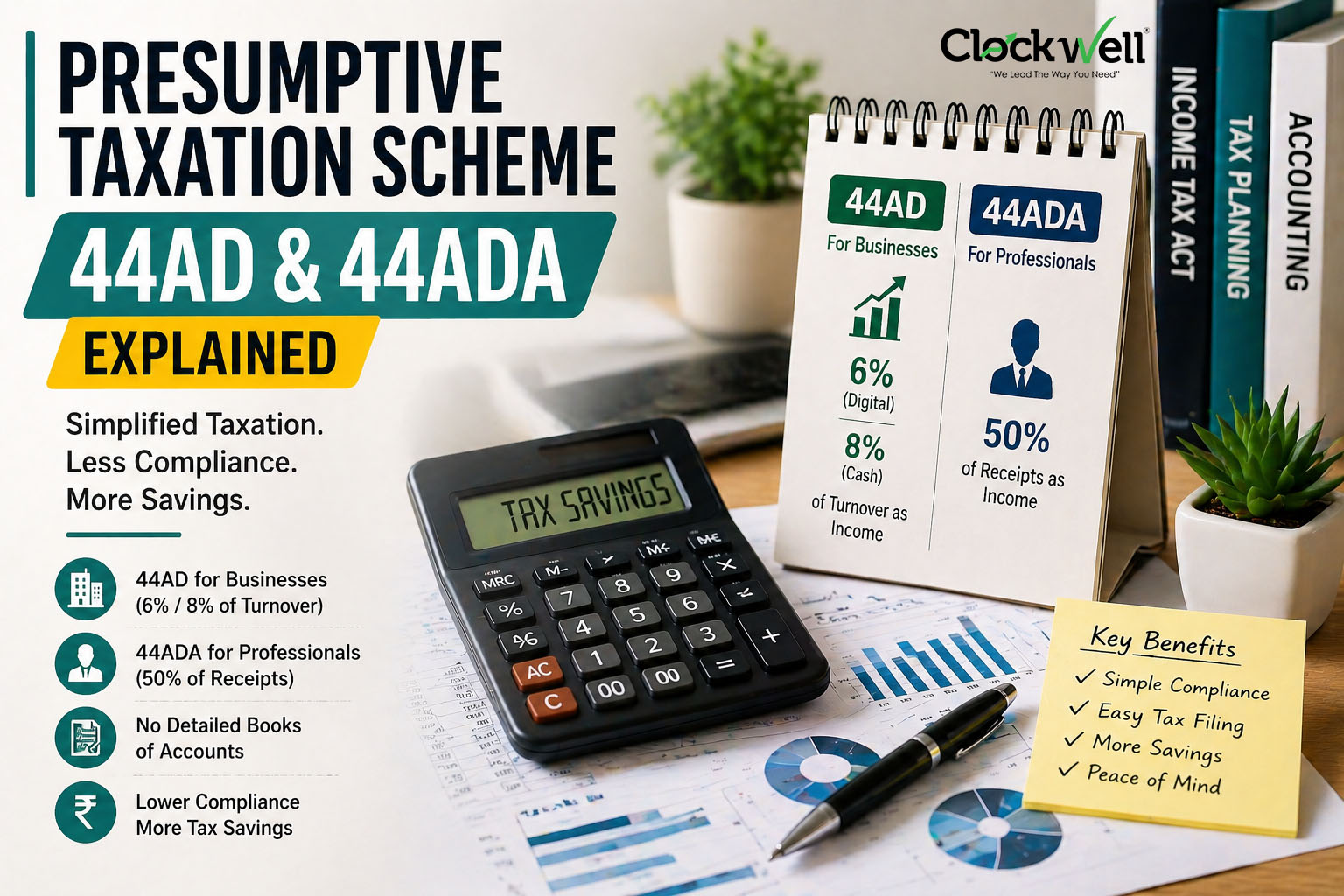

What is Presumptive Taxation Scheme?

The presumptive taxation scheme allows taxpayers to declare income at a fixed percentage of turnover or receipts, instead of maintaining detailed books of accounts.

This simplifies tax calculation and reduces compliance requirements.

Section 44AD – For Small Businesses

Section 44AD applies to small businesses.

Eligibility:

- Resident individuals

- Partnership firms (excluding LLP)

- Businesses with turnover up to ₹2 crore

Presumptive Income:

- 8% of total turnover (cash transactions)

- 6% of turnover (digital transactions)

You can declare income at these rates without maintaining detailed records.

Benefits:

- No need to maintain books of accounts

- No tax audit required (if conditions met)

- Simple tax calculation

Section 44ADA – For Professionals

Section 44ADA is designed for professionals.

Eligible Professionals:

- Doctors

- Lawyers

- Chartered accountants

- Architects

- Freelancers and consultants

Eligibility:

- Resident individuals or partnership firms

- Gross receipts up to ₹50 lakh

Presumptive Income:

- 50% of total receipts

This means half of your income is considered profit.

Key Differences – 44AD vs 44ADA

| Feature | Section 44AD | Section 44ADA |

|---|---|---|

| Applicable to | Businesses | Professionals |

| Turnover Limit | ₹2 crore | ₹50 lakh |

| Presumptive Income | 6% / 8% | 50% |

| Books of Accounts | Not required | Not required |

| Audit Requirement | Not required | Not required |

When Should You Choose Presumptive Taxation?

You should consider this scheme if:

- You want to avoid complex accounting

- Your actual expenses are low

- You prefer simple tax filing

- Your income fits within prescribed limits

When Not to Choose This Scheme

This scheme may not be suitable if:

- Your profit margin is lower than presumptive rate

- You want to claim detailed deductions

- Your turnover exceeds limits

- You need financial records for loans or investors

Important Rules to Remember

- Once opted, you must continue for 5 years (for 44AD)

- If you opt out early, restrictions apply

- Advance tax must be paid in one installment (15th March)

Understanding these rules is important before choosing the scheme.

Common Mistakes to Avoid

Many taxpayers misuse or misunderstand this scheme.

- Choosing scheme without proper calculation

- Ignoring turnover limits

- Not paying advance tax

- Mixing business and personal income

Avoiding these mistakes ensures compliance.

Benefits of Presumptive Taxation

Using presumptive taxation scheme 44AD 44ADA offers:

- Simplified compliance

- Reduced paperwork

- Lower accounting costs

- Faster return filing

- Less chances of errors

Impact on Freelancers and Small Businesses

This scheme is especially useful for:

- Freelancers

- Small traders

- Consultants

- Startup owners

It allows them to focus on business instead of complex tax processes.

How Clockwell Can Help

Choosing the right tax scheme requires proper analysis. A wrong choice can increase your tax burden.

Clockwell provides:

- Tax planning and advisory

- Income tax filing services

- Scheme selection guidance

- Compliance support

With expert help, you can choose the best option and save time and money.

The presumptive taxation scheme 44AD 44ADA is a powerful option for small businesses and professionals who want simplified taxation. It reduces compliance, saves time, and makes tax filing easier.

However, choosing the right scheme depends on your business structure and income level. Proper planning ensures maximum benefits.

Published on May 1, 2026