Starting a business is exciting, but many entrepreneurs focus heavily on sales, marketing, and growth while overlooking one critical area—financial management.

A great business idea alone does not guarantee success. In fact, many startups and small businesses struggle because of avoidable financial mistakes made during the early stages.

Understanding these common financial mistakes can help entrepreneurs build a stronger foundation, improve profitability, and increase long-term business success.

Why Financial Management Matters

Good financial management helps businesses:

- Maintain healthy cash flow

- Control expenses

- Avoid unnecessary debt

- Improve profitability

- Make informed business decisions

Without proper financial planning, even businesses with strong sales can face serious challenges.

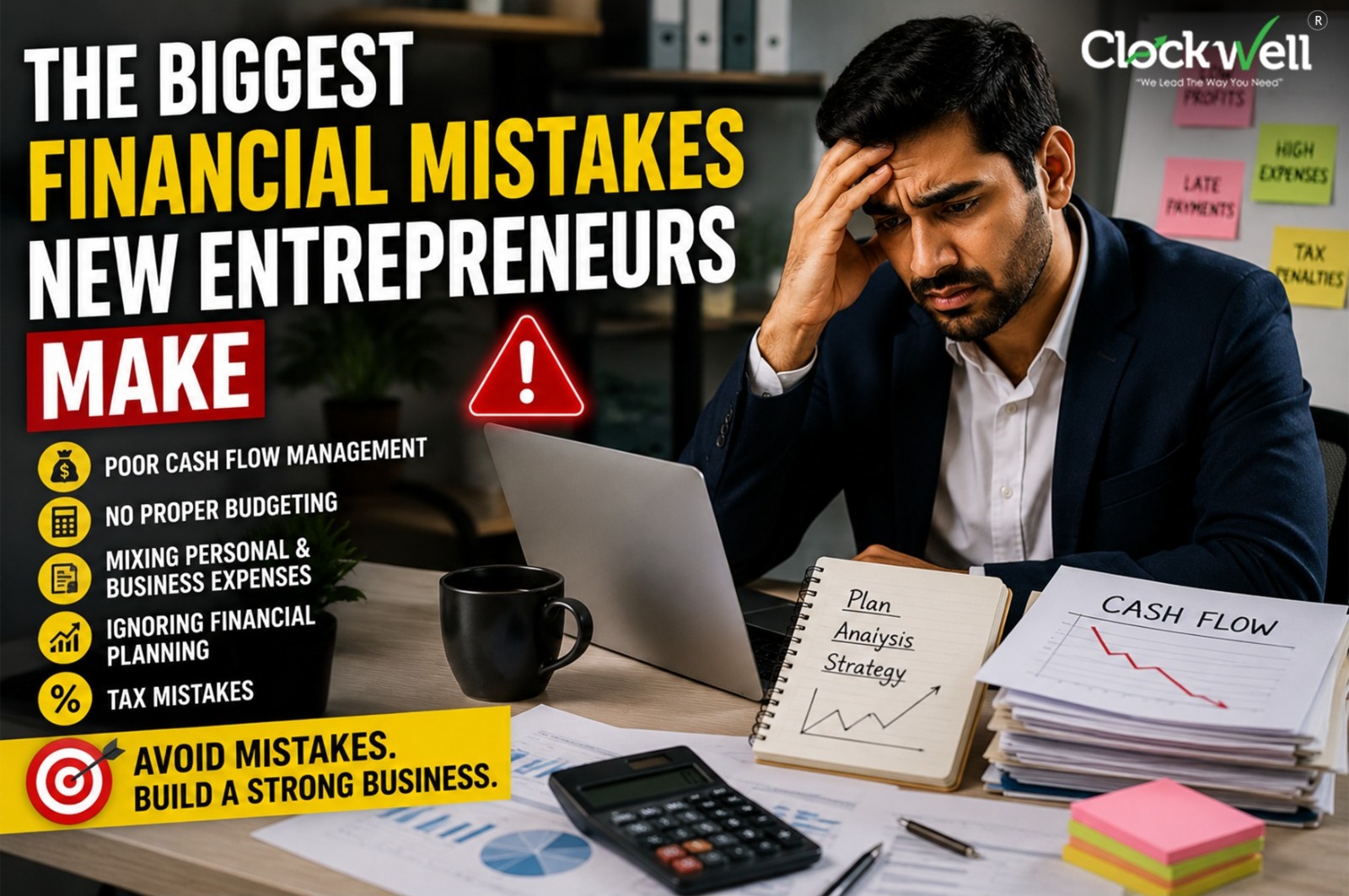

Biggest Financial Mistakes New Entrepreneurs Make

1. Mixing Personal and Business Finances

One of the most common mistakes is using the same bank account for both personal and business expenses.

Problems Created:

- Difficult bookkeeping

- Tax complications

- Inaccurate financial reporting

- Cash flow confusion

Always maintain separate business accounts from day one.

2. Ignoring Cash Flow

Many entrepreneurs focus only on sales and profit.

However, cash flow is often more important than profit.

A business can be profitable on paper but still struggle if cash is not available when needed.

Common Cash Flow Problems:

- Late customer payments

- Excess inventory

- Unplanned expenses

Regular cash flow monitoring is essential.

3. Not Maintaining Proper Accounts

Poor bookkeeping leads to poor decisions.

Without accurate financial records, business owners cannot clearly understand:

- Revenue

- Expenses

- Profitability

- Tax liabilities

Accurate accounting helps entrepreneurs make smarter business decisions.

4. Underestimating Startup Costs

Many new entrepreneurs budget only for initial setup expenses.

They often forget ongoing costs such as:

- Rent

- Salaries

- Marketing

- Software subscriptions

- Utilities

Proper budgeting helps avoid financial surprises.

5. Ignoring Tax Planning

Tax compliance is often treated as a year-end activity.

This approach can lead to:

- Penalties

- Interest charges

- Cash flow problems

- Tax notices

Regular tax planning helps businesses stay compliant and financially prepared.

6. Taking on Too Much Debt

Borrowing can support growth, but excessive debt creates financial pressure.

Risks Include:

- High interest costs

- Reduced profitability

- Cash flow strain

Entrepreneurs should borrow carefully and only when necessary.

7. Setting Incorrect Pricing

Many startups price products too low to attract customers.

While this may increase sales, it often reduces profitability.

Pricing should cover:

- Direct costs

- Operating expenses

- Profit margins

Sustainable pricing is crucial for long-term success.

8. Failing to Build an Emergency Fund

Unexpected events can affect any business.

Examples:

- Economic slowdown

- Equipment breakdown

- Market changes

- Customer payment delays

An emergency fund provides financial stability during difficult periods.

9. Making Decisions Without Financial Data

Many entrepreneurs rely on assumptions instead of numbers.

Important business decisions should be based on:

- Financial reports

- Cash flow analysis

- Profitability data

- Budget forecasts

Data-driven decisions reduce business risk.

10. Delaying Professional Financial Support

Many business owners try to manage accounting, taxes, compliance, and finances alone.

This often results in:

- Filing mistakes

- Compliance issues

- Missed tax benefits

- Poor financial planning

Professional guidance can save both time and money.

How Entrepreneurs Can Avoid These Mistakes

Create a Financial Plan

Set clear financial goals and budgets.

Track Cash Flow Regularly

Monitor incoming and outgoing cash.

Maintain Accurate Records

Use proper accounting systems.

Plan for Taxes

Prepare throughout the year.

Review Financial Reports Monthly

Regular reviews improve decision-making.

Seek Expert Advice

Professional support helps prevent costly mistakes.

Benefits of Strong Financial Management

Good financial practices help businesses:

- Improve profitability

- Increase cash flow

- Reduce financial risks

- Support business growth

- Maintain compliance

Financial discipline is often the difference between business success and failure.

How Clockwell Can Help

Clockwell provides:

- Accounting and bookkeeping services

- Tax planning and filing

- GST compliance support

- Financial reporting

- Business advisory services

Our experts help entrepreneurs build strong financial systems and make confident business decisions.

Many new businesses fail not because of poor products or lack of customers, but because of financial mistakes that could have been avoided.

By managing cash flow carefully, maintaining proper accounts, planning for taxes, and making data-driven decisions, entrepreneurs can build stronger and more sustainable businesses.

Smart financial management today creates a stronger business tomorrow.

Published on June 1, 2026